Exterior caulking is the first line of defence between your home’s structure and water infiltration, and its condition directly determines whether your insurer pays out or denies a water damage claim. Standard homeowners insurance policies exclude coverage for damage caused by a lack of exterior caulking maintenance. That single policy clause catches thousands of Canadian homeowners off guard every year. Understanding how exterior caulking affects insurance claims is not just useful knowledge. It is the difference between a covered repair and a bill you pay entirely out of pocket.

Why do insurance companies deny claims related to poor exterior caulking?

Insurers deny caulking-related claims by classifying the damage as a maintenance failure rather than a sudden, accidental event. Most standard homeowners policies cover sudden and accidental water damage. They do not cover damage that developed gradually because a homeowner failed to maintain the building envelope.

Adjusters look for brittle, cracked caulking as a pre-existing condition to exclude coverage. When an adjuster photographs deteriorated caulk around your windows or doors, that evidence supports a denial under the policy’s wear and tear exclusion. The insurer’s argument is straightforward: the damage was predictable and preventable.

Anti-Concurrent Causation clauses make this worse. ACC clauses allow insurers to deny claims if deferred maintenance contributed to the loss, even when a covered peril like a windstorm was also present. Courts have consistently upheld ACC clause enforcement when the policy language is clear. That places the burden squarely on you to prove your maintenance was current.

Common denial scenarios include:

- Water intrusion through a window frame where caulk has pulled away from the siding

- Rot in structural sheathing traced back to a failed caulk joint that was never replaced

- Interior drywall damage where the adjuster documents years of slow moisture migration

- Mould growth behind exterior cladding attributed to an unsealed expansion joint

Pro Tip: Request a written explanation of every denial and ask the adjuster to cite the specific policy clause. Vague denials are easier to appeal than ones tied to precise policy language.

How can homeowners document and maintain exterior caulking to support claims?

Proper documentation of exterior caulking condition is your strongest defence against a maintenance denial. Photographs and maintenance records reduce denial risk during storm damage claims where old caulk is involved. The goal is to show your insurer a clear, dated record of responsible upkeep.

Follow these steps to build a defensible maintenance file:

- Inspect annually. Walk the full perimeter of your property each spring and autumn. Check all caulk joints around windows, doors, penetrations, and expansion joints. Exterior caulk has a service life of 5–10 years, so track the age of every application.

- Photograph everything. Take wide-angle shots of each elevation and close-up shots of individual joints. Date-stamp every image. Store photos in a cloud folder organised by year and location on the building.

- Keep contractor invoices. Every professional caulking job should produce a written invoice describing the scope, materials used, and the date of completion. These records are direct evidence of maintenance.

- Use moisture testing after any water event. Thermal imaging and moisture meters are effective tools to prove active water migration and distinguish sudden damage from gradual deterioration. A licensed contractor or public adjuster can perform this testing and produce a written report.

- Select the right caulk type. Silicone-based sealants are recommended for wet and exterior environments. Using the correct product is part of demonstrating due diligence to your insurer.

Pro Tip: Hire a qualified caulking contractor every 7–10 years for a full building envelope inspection. A professional report on file is far more persuasive to an adjuster than your own notes.

Learning more about choosing a qualified contractor before you book an inspection will save you time and money.

What is the ensuing loss exception and how does it affect caulking claims?

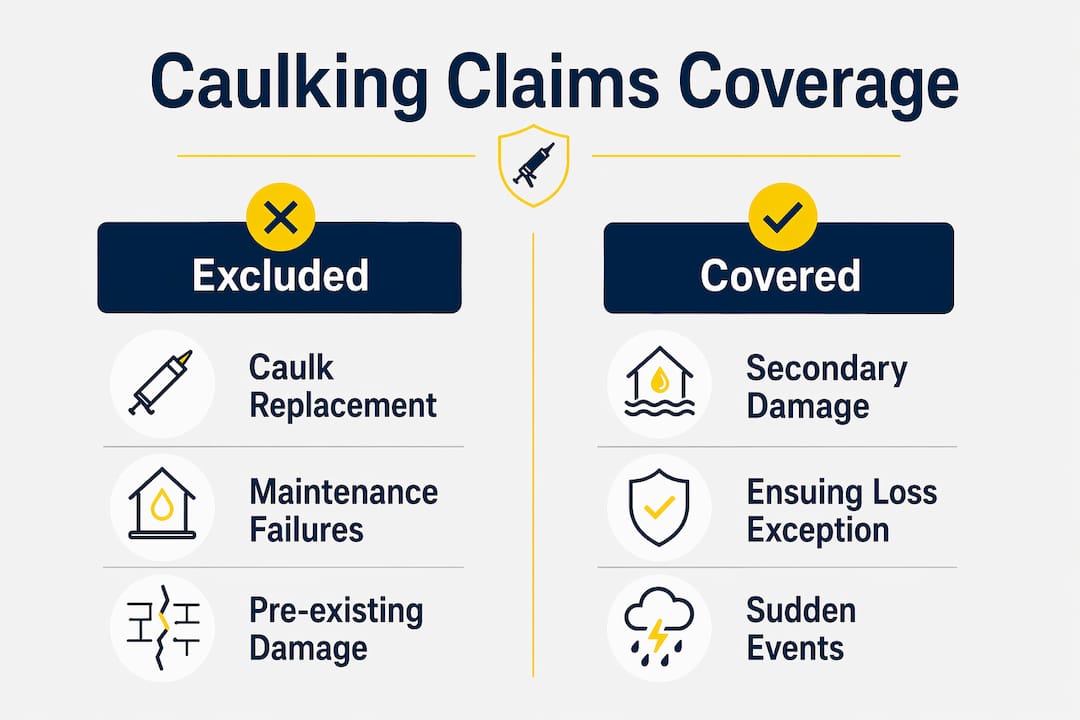

The ensuing loss exception is the most overlooked concept in property insurance, and it directly applies to failed caulking situations. Damage to structural elements caused by failed caulk may be covered even though the caulking repair itself is excluded. Many homeowners accept a full denial without realising this distinction exists.

The logic works like this. Your insurer can legitimately exclude the cost of replacing the deteriorated caulk. That is a maintenance item. However, if the failed caulk allowed water to reach your subfloor, rot your window framing, or damage your drywall, that secondary damage may qualify as an ensuing loss under a separate covered peril.

The table below shows how this distinction typically plays out:

| Damage type | Coverage status | Reason |

|---|---|---|

| Replacing failed exterior caulk | Excluded | Classified as routine maintenance |

| Rotted window framing behind failed caulk | Potentially covered | Ensuing loss from water intrusion |

| Damaged drywall from water migration | Potentially covered | Secondary damage from a covered peril |

| Mould remediation in wall cavity | Disputed | Depends on policy language and timing |

| Structural sheathing replacement | Potentially covered | Ensuing loss if damage was sudden |

Pro Tip: If your insurer denies the full claim, ask specifically whether the ensuing loss exception applies to the secondary damage. Get that question and their answer in writing.

Standard policies differentiate between excluded maintenance items and covered damage resulting from them. Knowing this distinction lets you push back on blanket denials with a specific, well-grounded argument.

What mistakes do homeowners commonly make with caulking and insurance claims?

Most claim problems are preventable. The errors below are the ones Kettlecontracting sees most often when homeowners call after a denial.

- Using interior caulk on exterior joints. Interior latex caulk is unsuitable for outdoor use. It breaks down quickly in Ontario’s freeze-thaw cycles. An adjuster who identifies the wrong product type can cite poor workmanship or a code violation as grounds for denial.

- Delaying maintenance until damage appears. Caulk does not fail overnight. Waiting until you see water stains inside the home means the deterioration has been visible from outside for years. That timeline works against you in a claim.

- Mischaracterising the damage when filing. Homeowners sometimes describe gradual water intrusion as a sudden event. Insurers are trained to spot signs of accelerated wear like brittle or missing caulk. Inconsistencies between your account and the physical evidence damage your credibility.

- Accepting the insurer’s preferred contractor without question. The insurer’s contractor works to the insurer’s estimate. That estimate may not reflect the full scope of damage. You have the right to get your own quotes.

- Ignoring the ensuing loss exception. Most homeowners accept a denial at face value. They do not know to ask whether secondary structural damage qualifies for separate coverage.

Understanding the role of caulk on your home exterior before damage occurs puts you in a much stronger position when a claim arises.

How to file a successful insurance claim involving caulking-related water damage

A well-prepared claim file is harder to deny. Follow these steps from the moment you discover damage.

- Stop further damage immediately. Apply temporary weatherproofing to any open joints or breaches. Insurers expect you to mitigate. Failing to do so gives them another reason to reduce your payout.

- Document before you repair. Photograph all visible damage, including the condition of the caulk at every affected joint. Wide-angle and close-up shots together tell a complete story.

- Order professional moisture testing. A moisture meter or thermal imaging report from a licensed contractor establishes that the water intrusion was active and measurable. This counters the “gradual wear” argument.

- Gather your maintenance records. Pull every invoice, inspection report, and dated photograph from your file. Present these proactively with your claim, not only if asked.

- Get an independent estimate. Detailed, itemised repair estimates from independent contractors improve claim negotiation. Do not rely solely on the insurer’s preferred contractor for scope or pricing.

- File promptly. Timely inspection, documented mitigation, and evidence gathering improve claim success. Delays weaken your file and give adjusters more room to argue the damage worsened due to inaction.

- Appeal in writing if denied. Reference the specific policy clause cited in the denial. Ask whether the ensuing loss exception applies to any secondary damage. Keep every communication in writing.

Independent contractor estimates are crucial to counter low-ball insurance offers that ignore the full extent of damage.

Key takeaways

Neglected exterior caulking gives insurers the grounds to deny water damage claims under maintenance exclusion clauses, making regular upkeep and thorough documentation your most effective protection.

| Point | Details |

|---|---|

| Maintenance exclusions are real | Insurers deny claims when failed caulk is classified as a maintenance failure, not an accident. |

| Document your upkeep | Dated photos, contractor invoices, and inspection reports counter adjuster denial arguments. |

| Know the ensuing loss exception | Secondary structural damage from failed caulk may be covered even when the caulk repair itself is not. |

| Use the right caulk product | Silicone-based exterior sealants are required; interior latex caulk can trigger a workmanship denial. |

| File promptly and independently | Timely filing and independent contractor estimates strengthen your claim and negotiation position. |

What 25 years of caulking in Oshawa taught me about insurance claims

I have seen the same situation play out more times than I can count. A homeowner calls after a water damage claim gets denied. I go out to look at the building and the caulk around the windows is grey, cracked, and pulling away from the frame. It has been like that for years. The insurer’s adjuster saw the same thing I did, and they used it to close the file.

The frustrating part is that the fix is not complicated. Exterior caulk on a typical Ontario home needs attention every 7 to 10 years. That is one professional visit per decade. The cost of that visit is a fraction of what a denied claim costs you in out-of-pocket repairs.

What I have also noticed is that homeowners who keep records almost always fare better. Not because the records are magic, but because they shift the conversation. When you hand an adjuster a folder with dated photos and contractor invoices, the “deferred maintenance” argument becomes much harder to make stick.

The ensuing loss exception is the piece most people miss entirely. I have watched homeowners walk away from legitimate secondary damage coverage because nobody told them to ask. If your claim gets denied, do not accept it as the final word. Ask specifically about the structural damage behind the failed caulk. That question alone has changed outcomes I have witnessed firsthand.

My honest advice: treat exterior caulking like any other scheduled maintenance on your property. Inspect it, document it, and replace it on time. It protects your building and it protects your claim.

— Felix

Protect your home and your claim with Kettlecontracting

Keeping your exterior caulking in good condition is one of the most direct ways to protect your insurance claim eligibility. Kettlecontracting provides professional residential and commercial caulking services across the Greater Toronto Area, using high-performance silicone-based sealants suited to Ontario’s climate.

Every Kettlecontracting job includes a thorough inspection of your building envelope, proper surface preparation, and materials that meet the durability standards insurers expect to see. Whether you need a full exterior re-seal or a targeted repair around windows and doors, the team delivers work that holds up through freeze-thaw cycles and stands behind your claim file. Contact Kettlecontracting to schedule an inspection and get a written report you can keep on file.

FAQ

Does failed caulking automatically void a water damage claim?

Failed caulking does not automatically void a claim, but it gives insurers grounds to deny coverage under maintenance exclusion clauses. Secondary structural damage caused by the failed caulk may still qualify under the ensuing loss exception.

How often should exterior caulking be replaced to satisfy insurance requirements?

Exterior caulk has a service life of 5–10 years. Replacing it within that window and keeping dated records of the work demonstrates the maintenance standard insurers expect.

Can I use any caulk product on exterior joints?

Silicone-based sealants are the correct choice for exterior use. Using interior latex caulk on exterior joints can be cited as poor workmanship or a code violation, which gives an insurer additional grounds to deny your claim.

What is the ensuing loss exception in a caulking claim?

The ensuing loss exception covers secondary damage caused by a maintenance failure even when the maintenance item itself is excluded. For example, rotted framing or damaged drywall behind failed caulk may be covered even though replacing the caulk is not.

Should I use the insurer’s contractor or hire my own?

You have the right to hire your own licensed contractor. Independent, itemised estimates from a qualified contractor improve your negotiating position and often capture damage that the insurer’s preferred contractor underestimates.